Will Insurance Cover My Vein Treatment?

Many patients assume that vein treatments are considered cosmetic and thus not covered by health insurance, but that is not true.

Consultation and UltrasoundThe first step is to go for a consultation with the doctor. During the visit, he examines you and evaluates your venous disease and general health. At the same visit, he measures vein sizes and reflux times (the amount of time it takes for valves in the veins to close) using an ultrasound. When the valves don’t close correctly, the blood pools in your legs—causing swelling, pain, and varicose veins. The results of the consultation and ultrasound will be sent to your health insurance provider to gain approval for the recommended treatments.

Conservative TreatmentThe insurance company will typically request that the patient try a conservative treatment plan to see if ablations can be avoided. Compression stockings, elevating the legs, and over-the-counter pain medication will be used for a period of anywhere from two weeks to three months (depending on what your insurance company requests). For most patients, the symptoms persist, proving to the insurance company that there has been a “Failure of Conservative Treatment.”

Medical NecessityNow the insurance company will likely preauthorize the vein treatment and cover the costs, based on the parameters of your plan.

Out-of-Pocket CostsOnce your treatment plan is approved, the team at Fitzgibbons Vein Center will help determine how much you will have to pay and how much will be paid by your health insurance company.

Note that actual dollar figures and percentages depend on your specific plan. Deductibles, coinsurance, and copays are all examples of “shared costs,” the costs that you share with your insurance company. It’s important to understand these health insurance “buzzwords.”

- Deductible: You will pay for all medical costs up to the cost of your deductible. After the deductible is met, your health insurance company will start to cover some costs.

- Coinsurance: Your plan specifies a specific coinsurance level. For example, once the deductible is met, your health insurance company might cover 95% of all costs. You will pay the 5% left. The actual percentage varies depending on your plan.

- Copay: A copay is a set amount that you pay for doctor or pharmacy visits.

- Annual Out-of-Pocket: Your health plan also has a specific annual out-of-pocket amount. Your deductible, copays, and coinsurance add up, and once the total hits this amount, your health insurance will cover all additional costs.

- Secondary Insurance: Consumers can opt to purchase secondary insurance as well. This supplemental plan will cover the shared costs of your primary insurance.

- PPO vs. HMO: PPOs (preferred provider organizations) and HMOs (health maintenance organizations) are two different types of insurance plans. The main difference is that if you have an HMO, you’ll need to get a referral from your primary care physician. Fitzgibbons Vein Center is an approved provider for all major PPOs, many HMOs, Medicare and Medi-Medis.

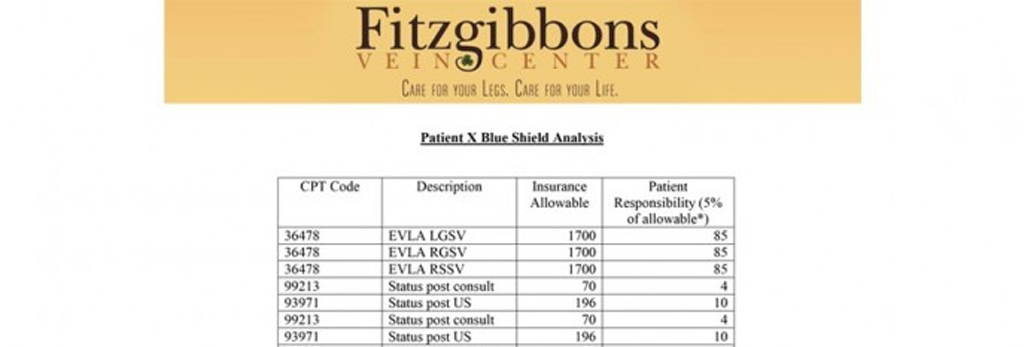

Because this information can be confusing, the staff at Fitzgibbons Vein Center will create a free personalized spreadsheet showing your treatment plan, what you can expect to pay, and how much will be covered by your insurance (sample pictured). Of course, always double-check the amounts with your insurance company.

To learn more or to schedule a consultation, call 213-785-8333.

...